iSmartNetwork Magazine The online magazine for you…

iSmartNetwork Magazine The online magazine for you…

Here’s what debt to asset ratio means 😛 TAGEND

When you’re a business( i.e. you have your own business or back hustle ), your obligation to asset ratio represents the total amount of obligation you owe compared to your total amount of assets.

This influences how much lenders will be willing to give you AND helps you be aware of how much you owe to creditors.

If you’re an individual, the debt to asset rate won’t be as relevant to you…but your debt to INCOME ratio will be. That’s the amount representing the total amount of debt you owe compared against your income.

Mortgage lenders, bank loan, and anyone giving you credit will take a look at your indebtednes to asset/ income ratio in order to determine how much they’re willing to be provided to you.

Your debt to asset rate( or debt to income ratio) could intend the difference between securing a lend for your business or residence, and not getting a single dime from a lender.

To help you get a better understanding of it, let’s break down what obligation to asset ratio might look like in real life.

Clarify Like I’m 5: Debt to asset ratio

Let’s say an unemployed acquaintance of yours, we’ll call him Jeff, asks to borrow $10 from you.

What do you do?

Immediately, with your $10 in your hand, you’ll ask yourself a bunch of questions about Jeff, including 😛 TAGEND

“Do I trust Jeff? ” “Will Jeff paid in full back? ” “Whoa, why is the guy from Hamilton on the $10? ”

Hard to answer these questions, right? Now pretend a third person, your mutual pal Mary, tells you that Jeff borrowed $100 from her last week and hasn’t paid it back. Now what do you do?

You slip your $10 back in your pocket and move on.

In a nutshell, this is debt to asset ratio.

However, that’s not the only debt ratio you need to understand. In IWT fashion, we’re going to give you the rundown on three indebtednes rates that are going to matter the most to you, your life, and/ or your business. They are 😛 TAGEND

Debt to asset rate Debt to equity rate Debt to income ratio

It’s so important to keep these numbers in psyche be informed about your indebtednes( if you have any that is ), because when they’re out of whack they can stifle your ability to establish some large-scale purchases.

Debt to asset rate: Important for businesses

( NOTE: If you’re not a small business owner or don’t run your own side hustle, you can skip down to debt to income rate .)

Like your credit rating, your indebtednes to asset ratio is a number. One that goes to show how much of your resources — things like your cash, investments, inventorying, etc. — be payable with indebtednes, including 😛 TAGEND

Credit cards Bank lends Student lends Mortgages

( Pretty much any instance that you owe fund to someone .)

The way you calculate your obligation to asset rate is simple: Take the amount of obligation you owe and subdivide it by the value of the assets you own. Then, take that number and multiply it by 100 so you get a percentage. That’s your debt to asset ratio.

It’ll look something like this:

Dollar amount of indebtednes you owe/ Dollar amount of resources you own= Debt to asset ratio

And then 😛 TAGEND

Debt to asset ratio x 100= Debt to asset ratio percentage

It’s genuinely that simple.

What is a good debt to asset ratio?

The higher your debt to asset rate is, the more you owe and the more risk you run by opening up new pipelines of credit.

According to Michigan State University professor Adam Kantrovich, any rate higher than 30%( or. 3) may lower the “borrowing capacity” for your business. That’s why it’s so smart-alecky for you — especially if you’re a business owner or freelance — to know your indebtednes to asset ratio.

However, the amount your obligation to asset rate affects your business will vary from industry to industry.

For example, enterprises that present internet services generally don’t require a lot of debt up front to start. That means they’ll generally have lower indebtednes to asset ratios on average.

However, industries such as production or retail require a LOT of indebtednes up front in order to get started. As a answer, it’s not uncommon to see higher debt to asset ratios among them.

Check out the chart below to find out the average debt to asset rate in a few different industries.

Industry Average debt to asset ratio

Internet services and social media 25% Consumer electronics 34% Energy 108% Technology 110% Utilities 228% Retail 289%

From CSI Market( a market analysis company)

“Holy crap, Ramit! Why are firms like utilities and retail so high-pitched? ”

Businesses like utilities and retail require a whole lot of initial capital up front to cover initial costs of things they need to run their business( infrastructure, products, manpower, etc .). As such, the average debt to asset ratio for those working industries will be higher.

Many lenders such as banks and mortgage corporations may take this into consideration when they’re lending to you and your business.

Say you’re a small business owner looking to get a new loan for your undertaking. After totaling everything up, you find that you owe about $25,000 in debt and own about $100,000 in assets.

After dividing your obligation by your resources and multiplying that number by 100, you discover that your indebtednes ratio is 25% — which is just about the average if you work in internet services and stellar if you work in retail.

However, if those numbers were flip-flop( you owe $100,000 in debt and own only $25,000 in assets ), your indebtednes to asset amount would be 400% — which is just awful no matter what your business does.

A tone on indebtednes to equity rate

Sometimes, lenders will look at a business’s debt to equity ratio instead. Lucks are this doesn’t apply to 99.999% of you. But so you are familiar, obligation to equity looks at a company’s debt compared to shareholder equity( the value of the shares) and is calculated the same way as obligation to asset ratio 😛 TAGEND

Dollar amount of debt you owe/ Dollar amount of shareholder equity= Debt to equity ratio

And then 😛 TAGEND

Debt to equity rate x 100= Debt to equity ratio percentage

Like debt to asset ratio, your debt to equity ratio will differ from business to business.

However, general consensus for most industries is that it should be no higher than 2( or 200% ).

“But Ramit, I don’t have a big company or business. Does any of this matter to me? ”

Yes! Because there’s a formula that both creditors and lenders use to assess the risk of individuals like you.

Debt to income ratio: Important for individuals

If you plan on ever get a mortgage for a house, you need to make sure your debt to income rate is in check.

This number compares your gross monthly income to your monthly debt. Banks and other lenders look at this number to determine how much of a risk you are to lend to. The more of a risk you are, the less of a chance they’ll lend to you at all.

Much like your debt to asset rate, calculating it is simple 😛 TAGEND

Dollar amount of monthly indebtednes you owe/ Dollar amount of your gross monthly income= Debt to income ratio

And then 😛 TAGEND

Debt to income rate x 100= Debt to income rate percentage

Let’s run an example scenario 😛 TAGEND

Say you owe about $1,000 in debt month-to-month and construct $75,000 a year ($ 6,250/ month ). We’d then take 1,000 divided among 6,250 in order to get our obligation to income rate, like so 😛 TAGEND

1, 000/ 6,250=. 16

Multiply. 16 by 100 and you have 16% for your obligation to income ratio….but what does that amount mean?

What is a good debt to income rate?

The lower the number is, the better. According to Wells Fargo, the ideal debt to income ratio is 35% and below. That said, most lenders will provide you a loan up to 43 -4 5 %.

So if your debt to income rate amounted to 16% like in the lesson above, you’d be in good shape for a home loan.

If your obligation to income rate is a little higher and you want to lower it, though, I’d like to help you out.

After all, being in debt is the# 1 hindrance to living a Rich Life, and not only is it a financial onu, but it can also be a HUGE psychological onu as well.

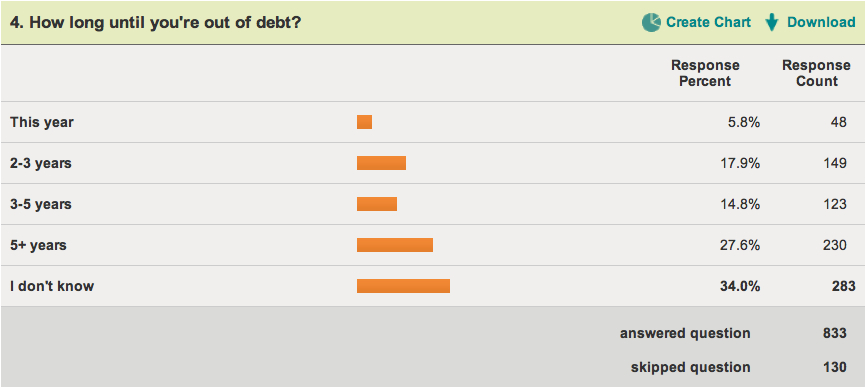

For example, a while back I passed a survey of my readers who were in debt, asking them a apparently simple question: How long until you’re out of debt?

Take a look at the results 😛 TAGEND

34%( the majority of members) of respondents DIDN’T KNOW how long it would take until they were out of debt.

Debt is just as much of an emotional issue as a fiscal one. That’s why throwing a personal finance book at someone in debt or depicting them a obligation calculator develops little to no change.

If someone’s too afraid to even open the envelopes that will tell them how much they owe, “information” is not what they need. Instead, that person has to be willing to take action THEMSELVES before anything will change.

If you’re reading this now, and you’re ready to take action against your obligation, I want to help you.

In fact, you can start getting out of debt TODAY through a 5-step structure I’ve developed.

Just check out my popular article on how to get out of debt here.

Get out of debt and live a Rich Life

So that’s your debt to asset ratio. It’s a good way to keep an eye on your personal finances and an element to consider if you had wished to get a loan.

But eliminating debt is just the first step on the expedition to living a Rich Life.

If you want to learn my best strategies for creating multiple income torrents, starting a business, and increasing your income by thousands of dollars a year, download a free transcript of my Ultimate Guide to Making Money below.

Just enter your name and email below to get instant access to the Ultimate Guide to Making Money.

How to calculate your indebtednes to asset ratio (+ check if it’s good ) is a post from: I Will Teach You To Be Rich.

Read more: iwillteachyoutoberich.com